Intelligent counter fraud management for the digital bank

Intelligent counter fraud management for the digital bank

Actions

Intelligent counter fraud management for the digital bank

Based on industry estimates in 2016 the top 10 fraud types alone account for $181 Billion in annual losses. And the numbers will keep increasing across most fraud types and in 2018 more than 300 Billion in annual losses are expected. Banks are in serious trouble as new fraud patterns continue to emerge. Digital transformation opens many new opportunities for business and revenues, but that also accounts for new ways to penetrate the system.

Some background on counter-fraud

First generation payment fraud prevention solutions used coded expert experience. They use velocity counters and expert rules to identify high-risk behaviour. While the upside of this approach lies in its simplicity, the ever increasing number and complexity of fraud patterns have rendered it less and less efficient.

Second generation solutions generate fraud detection models from past payment and fraud data. Neural networks and advanced statistics used for this typically require the collection of large amounts of data over a long period. This data is then sent to the vendor to create a model off site. By the time the (re)trained model is delivered back and put into production, the fraud patterns it attempts to detects can be up to a few years old. It takes over 4 weeks to discover a new pattern, then another 4 weeks to adjust the scoring engines. The loss exposures remain until counter measure are in place.

The IBM Safer Payments is a third generation counter fraud management. It uses interactive machine learning from past data. However, rather than generating a black box model, it generates easily readable expert rules/scenarios. Based on artificial intelligence, which operates on decades of human experience in its creation of fraud prevention rules/scenarios, third generation solutions like Safer Payments can generate new or revised models with considerably less data, and with much faster model update cycles.

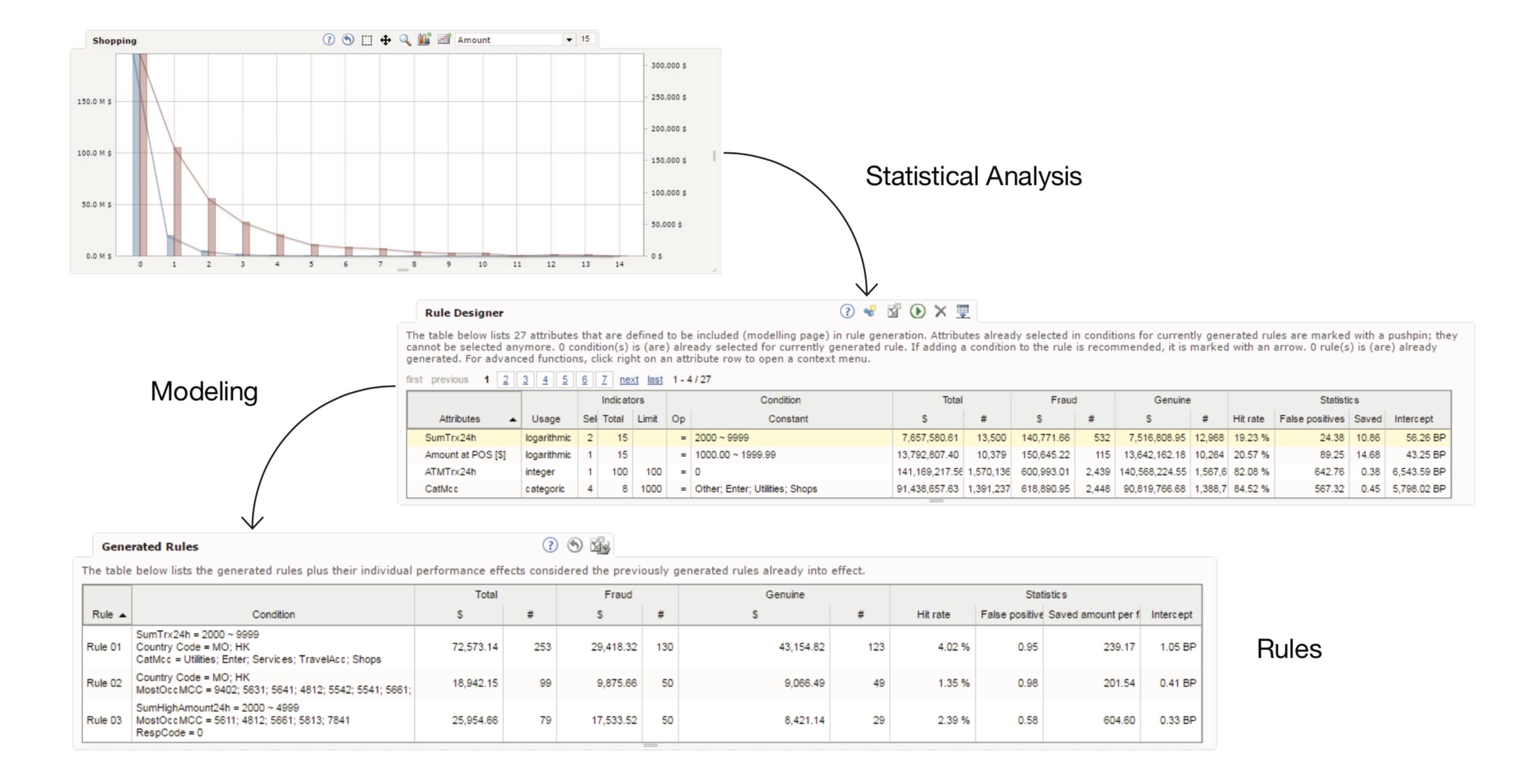

Statistics vs. Real-time Machine Learning

Neural networks and advanced statistical methods require massive amounts of training data to create a stable model that does not overfit. Frequently the amounts of data that individual payment processors can provide for this is not sufficient. Born out of necessity, neural network vendors have thus created the concept of the “consortium model”, where they pooled data from multiple processors to create a model.

While this has worked somewhat well in the past in homogenous markets, consortium models fall short in today’s dynamic environments. In smaller payment markets, fraud patterns are rather regional and thus blending data from multiple processors results in low detection rates and too many false positives. In larger payment markets, fraud patterns tend to become more and more “individual” by processors, so consortium models also become less and less effective.

In direct comparison, the cognitive approach with Real-time Machine Learning yields stable models with much less data than neural networks require. This means that even a small or medium sized payment processor to afford a custom model. Optimized for the fraud patterns this processor experiences, a custom model generates higher fraud hit rates and lower false positives.

As an added benefit, the fact that model updates – such as adaptations of an existing model to emerging fraud patterns – require very little new data, the artificial intelligence approach also allows to update models within hours of a new pattern emerging.

Simulation, analysis and modeling

IBM Safer Payments comprises all analytics and simulation tools needed to continuously monitor the business performance of IBM Safer Payments, and to adapt the decision model to emerging and modified fraud patterns. It continuously monitors the efficacy of all defined fraud countermeasures and decision rules, highlighting the ones that demonstrate declining performance over time to the fraud experts for review.

At the same time, IBM Safer Payments’ artificial intelligence algorithms devise new fraud countermeasures and rules automatically from its internal database and presents them to the users for review.

New threats requires new protection

Online and mobile banking are attacked by phishing schemes, malware, and cybercrime. The challenge is to both provide security from fraud, but at the same time ensuring prime customer experience. Safer Payments is the right solution here because it profiles transactions, identifies counterparties and devices, identifies malware – all in the background – never disturbing the customer or putting additional security steps in the way. Only when Safer Payments identifies a high risk transaction, will it become the subject of further scrutiny and may be subject to step-up authentication. This approach also provides compliance with various regulations, such as the payment system’s directive (PSD2) issued by the European Central Bank.

Contact us if you need more information or would like to set up a test or Proof-of-Concept project or generally consult about digital transformation and/or PSD2 regulation requirements.

IBS (Email Application Registration)

Actions